Would you rather earn an annual return of 11.5% on your money or 5.4%?

If the answer to that question is a no brainer, why do so many investors choose an asset allocation strategy that earns them only 5.4%?

If you followed the 60/40 asset allocation strategy over the past 20 years, you likely earned around a 5.4% annual return on your money. And if you stick with it over the next 10 years, you’ll make even less.

What is the 60/40 strategy?

According to a recent Forbes article, the 60/40 strategy has been one of the most dominant investment approaches over the last 92 years. It’s been a popular approach because it’s been a favorite of Wall Street brokers and advisors who they can put their clients’ portfolios on autopilot using this strategy – freeing up time to prospect the next ten suckers they can market the same approach to.

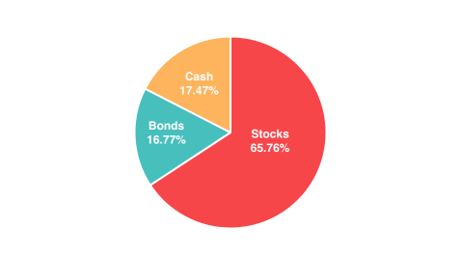

With the 60/40 rule, the broker or advisor allocates 60% of your assets to stocks, and 40% is allocated to a mix of bonds and cash. It’s simple and easy to explain. That’s why it’s so popular with brokers and advisors. It can be mass-marketed.

According to the latest asset allocation survey by the American Association of Individual Investors, here is how individual investors allocated their assets:

The idea behind the 60/40 allocation rule is that if stocks go down, bonds – which traditionally moved in the opposite direction of stocks – would pick up the slack to preserve the portfolio. This may have worked in the ’80s when treasury rates hovered near 10%, but that rule no longer makes sense today where the 10-year treasury currently sits at 0.96%.

If you stick with a 60/40 asset allocation over the next decade, you will barely keep ahead of inflation.

Morgan Stanley recently put out a report projecting the returns from a 60/40 portfolio to be just shy of 3% a year over the next decade. The average annual inflation over the past 30 years has been around 2.5%. Taking into consideration inflation, that’s a projected net annual return of 0.5% per year over the next decade.

Will you be satisfied with a 0.5% annual return over the next decade? If not, then it’s time to reevaluate your portfolio and consider an asset reallocation.

I asked you at the beginning of this article if you would rather make 11.5% on your money or 5.4%. Who wouldn’t want to make more than double on their money?

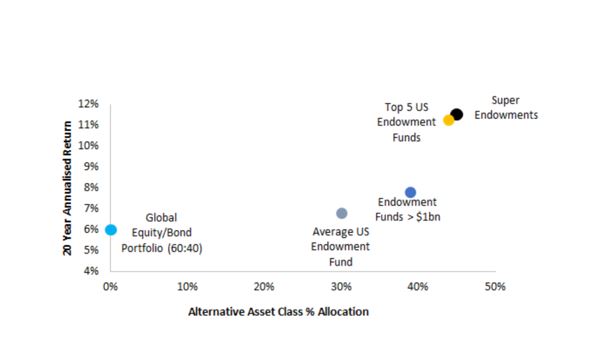

But what kind of asset allocation would yield an 11.5% return? What kind of investor is earning 11.5% annual returns? University endowments like Yale and Harvard are.

How are they earning these returns? By allocating nearly half of their assets to cash-flowing alternative assets like real estate, private equity, and fixed-income private debt.

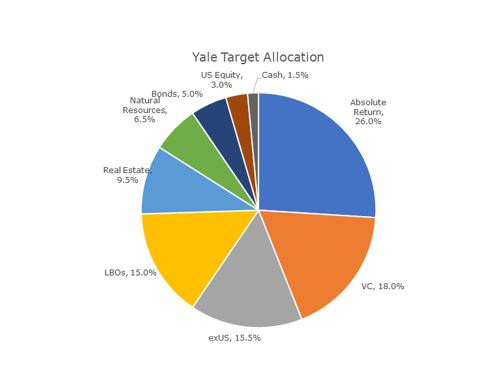

Check out Yale’s asset allocation:

Instead of allocating 60% to stocks and 40% to bonds, Yale only allocates 3% to each of those asset classes. The value of income-producing alternative investments cannot be overstated. The universities that allocated a higher percentage of their assets to alternatives saw better returns on their money.

Why are institutional investors like the Yale Endowment so aggressive in investing in alternative assets?

Because their priorities are different from individual investors who are only interested in the growth of their portfolios so they have enough at retirement. The Yale Endowment, currently valued at $31.2 billion, has different priorities.

Their two main objectives are:

- To generate enough cash flow to meet current operating expenses.

- To grow capital for future generations.

Why Cash Flowing Alternative Assets?

Cash flowing alternative assets are ideal for meeting current financial needs while building multi-generational wealth because part of the cash flow can be reinvested to generate multiple streams of recession-resistant income due to noncorrelation to Wall Street.

Would you like to generate the type of returns that would allow you to meet your current financial needs while building long-term wealth?

Then maybe it’s time to reevaluate and reallocate your portfolio.

Do you have the allocation you’ll need to earn 11.5%? Not if you’re working with brokers or advisors. The Wall Street darling 60/40 allocation is simply not going to cut it. It hasn’t cut it for the past 30 years.

While individual investors have been content to make 5.4% the past 20 years from the 60/40 allocation, institutional investors like the Yale Endowment have been plugging away making 11.5% from investing in alternatives.

If your goal is to generate income from your investments while profiting from appreciation and reinvestment, it’s time to consider cash flowing alternative investments like real estate, private equity, and fixed-income private debt.

kuhnya_jeKn

Идеальная кухня на заказ для вашего дома, у опытных дизайнеров.

Преобразите свою кухню с помощью индивидуального заказа, воплотим ваши фантазии в реальность.

Уникальные решения для вашей кухни на заказ, эксклюзивно для вас.

Индивидуальный заказ кухни, который порадует вас каждый день, не упустите свой шанс.

Создайте уют и комфорт на своей кухне с помощью заказа, получите неповторимый дизайн.

Эксклюзивная кухня, созданная специально для вас, лучший выбор для вашего дома.

Индивидуальный дизайн кухни, который порадует вас каждый день, наслаждайтесь каждым моментом на своей новой кухне.

Мы создаем кухни на заказ, которые радуют глаз, сделано с душой.

кухня на заказ https://kuhny-na-zakaz-msk.ru/ .

AmaliaAK

Натяжные потолки в Москве

CadeElilup

pret 5500 euros

arenda_apMt

Аренда автобуса в СПб: надежно и удобно, арендовать для поездки.

Оптимальные цены на аренду автобуса в СПб, пользуйтесь нашими услугами.

Лучшие автобусы для аренды в СПб, перевозите группу с комфортом.

Аренда автобуса для торжества в Санкт-Петербурге, с легкостью.

Трансфер из аэропорта с арендованным автобусом в СПб, пунктуально и качественно.

Организация корпоратива с арендованным автобусом в Санкт-Петербурге, профессионально и креативно.

Отдельный тур на автобусе в СПб, ярко и насыщенно.

Организуйте школьную экскурсию с арендованным автобусом в СПб, интересно и разнообразно.

Аренда автобуса для свадьбы в СПб, стильно и празднично.

Как выбрать автобус для аренды в СПб, подсказки от наших экспертов.

Способы сэкономить на аренде автобуса в Санкт-Петербурге, с максимальной выгодой.

Какие услуги включены в аренду автобуса в СПб, ознакомьтесь перед заказом.

Преимущества аренды автобуса с шофером в Санкт-Петербурге, честный рейтинг.

Сравнение стоимости аренды автобуса в СПб: как выбрать выгодное предложение, важные аспекты.

Аренда минивэна в СПб для небольших групп, легко и практично.

Прокат автобуса для музыкального фестиваля в СПб, безопасно и комфортно.

Аренда автобуса для корпоративного веселья в Санкт-Петербурге

аренда микроавтобуса спб https://arenda-avtobusa-v-spb.ru/ .

chto_orpt

Что такое роза и почему она так ценится, цветок, который украшает сады и сердца.

Какие бывают виды роз, секреты выращивания роз в домашних условиях.

Значение розы в разных культурах, тайны и загадки розы.

Роза как идеальный подарок для любого случая, какие чувства вызывает роза у людей.

Розы в архитектуре и дизайне интерьера, изысканные букеты из роз для особого случая.

про розу https://roslina.ru/ .

Richardpak

https://namazit.ru/

kotel_tpOi

Лучшие котлы для отопления частного дома | Какой котел для отопления дома выбрать | Лучшие цены на котлы для отопления | Эффективный выбор котла для отопления частного дома | Секреты установки котла для отопления | Выбор лучшего котла для отопления частного дома | Где купить котел для отопления частного дома с доставкой | Лучшие котлы для отопления: какой выбрать? | Секреты экономичного отопления частного дома | Где купить недорогой котел для отопления

купить котел для отопления частного https://sauna-manzana.ru/ .

AmaliaOP

Натяжные потолки цена

AnthonyElilup

lopressor pills

shkaf uqon

Уникальный шкаф купе на заказ с учетом ваших предпочтений

купе на заказ https://shkaf-kupe-nazakaz177.ru/ .

WilliamDek

娛樂城體驗金

富遊娛樂城體驗金使用規則與遊戲攻略

在富遊娛樂城,體驗金為新會員提供了一個絕佳的機會,讓你能夠在不冒任何財務風險的情況下,體驗多種精彩的賭場遊戲。然而,要將這些體驗金轉換成可提現的現金,需要達到一定的投注流水條件。

體驗金使用規則

活動贈點: 新註冊會員可獲得168元體驗金。

活動流水: 未儲值前需達成36倍的投注流水,儲值後僅需1倍流水即可申請提款。

參加資格: 每位新會員限領一次體驗金。

申請方式: 只需加入富遊客服官方LINE,即可領取體驗金。

遊戲推薦與最佳利用體驗金

百家樂: 這是體驗金玩家的首選,最低投注額僅需20元,讓你能在多次投注中累積流水,達到提款要求。

彩票彩球: 超低投注門檻(1至10元)讓你在體驗的同時,也有機會贏得大獎。

運彩投注: 用100元體驗金來預測賽事結果,不僅享受觀賽的刺激,還有機會贏得獎金。

棋牌遊戲: 最低投注額僅需1元,適合喜愛棋牌遊戲的玩家。

電子老虎機: 只需0.2至1元的投注額,即可輕鬆轉出驚喜獎金。

為何選擇富遊娛樂城?

安全至上: 採用先進的加密技術,確保個人資訊與資金的安全。

遊戲多元: 提供豐富的遊戲選擇,包括老虎機、百家樂、撲克、彩票、運彩等。

貼心客服: 專業客服團隊24小時在線,隨時解決你的問題。

獨家APP: 隨時隨地都能玩,娛樂不間斷。

富遊娛樂城專注於提供公平的遊戲環境,所有遊戲結果均由隨機數字產生器決定,保障每位玩家的公平性。同時,透過富遊APP,玩家可隨時隨地享受多種經典賭場遊戲。

結語

無論你是新手還是老玩家,富遊娛樂城的體驗金活動都能讓你在享受遊戲的同時,體驗到賭場的刺激與樂趣。立即註冊,領取你的168元體驗金,開始你的遊戲之旅吧!

shkafy_kbOl

Идеальные шкафы купе на заказ в Москве, Создайте свой шкаф купе мечты в Москве

шкаф купе на заказ москва https://shkafy-kupe-na-zakaz77.ru/ .

GeorgeBoamp

top 10 nhà cái uy tín

Dưới đây là văn bản với các từ được thay thế bằng các cụm từ đề xuất (các từ đồng nghĩa) được đặt trong dấu ngoặc nhọn :

Hàng đầu 10 Nhà khai thác Uy tín Bây giờ (08/2024)

Cá cược trực tuyến đã biến thành một mốt rất thông dụng tại Việt, và việc chọn ra nhà cái đáng tin tưởng là vấn đề hết sức cần thiết để đảm nhận cái trải đánh bạc không rủi ro và công bằng. Bên dưới là danh sách Mười ông lớn nhà cái đáng tin số một hiện tại, được phổ biến bởi trang đánh giá hàng đầu Danh sách 10 ông lớn.

ST666 được xem là một trong những nhà cái lớn kết hợp với uy tín hàng đầu ngày nay. Cùng với chăm sóc khách chuyên nghiệp, hỗ trợ không ngừng kết hợp các gói ưu đãi đặc sắc như thể thưởng 110% lúc nạp lần đầu, tất cả khẳng định là lựa chọn hàng đầu với khách hàng.

RGBET nổi bật hơn cùng với dịch vụ cam kết thất bại thể thao lên đến 28,888K, cùng với hoàn lại game slot 2% không ngừng. RGBET chính là lựa chọn hoàn hảo cho mọi người yêu thích chơi game thể thao và trò chơi đánh bạc.

KUBET được nhắc đến bên cạnh hệ thống an toàn vượt trội và máy chủ chuyên biệt, trợ giúp bảo vệ tối đa dữ liệu người sử dụng. Nhà cái này cung cấp nhiều dịch vụ giảm giá lôi cuốn như nạp lần hai, giảm giá 50%.

BET365 đại diện cho nhà cái cá cược thể thao ưu việt trên châu Á, vượt trội kèm theo các kèo châu Á, cược tài xỉu và live thể thao. Nó chính là chọn ra lý tưởng dành cho những người thích thú cá cược thể thao.

FUN88 không đơn thuần sở hữu tỷ suất thưởng hấp dẫn nhất song cũng sở hữu nhiều gói giảm giá riêng biệt như thể ưu đãi 108K Freebet và vé cược thể thao SABA tới 10,888K.

New88 lôi cuốn người tham gia cùng với các ưu đãi khuyến mãi lôi cuốn tương tự như hoàn lại 2% miễn phí và chiêu đãi lì xì mỗi ngày. Chúng đại diện cho một trong những cái nhà cái đang đón nhận đa dạng sự quan tâm của khách hàng đánh bạc.

AE888 nổi trội với dịch vụ trao 120% lần ban đầu nạp đá gà

Vâng, tôi sẽ tiếp tục từ đoạn cuối của văn bản:

AE888 vượt trội kèm theo chương trình trao 120% lần đầu tạo tài khoản cá cược gà và các dịch vụ khuyến khích hấp dẫn đặc biệt. Tất cả là nhà cái độc quyền đưa ra không gian SV388.

FI88 chiêu dụ người tham gia bên cạnh tỷ lệ hoàn lại vượt trội bên cạnh các ưu đãi thưởng tạo tài khoản hấp dẫn. Tất cả chính là tuyển chọn vượt trội với tất cả thích thú casino trực tuyến và game slot.

F8BET nổi bật hơn kèm theo chương trình tặng nạp khởi đầu nhận được 8,888,888 VNĐ kèm theo cùng với nhà quản lý tiền thưởng 60%. Tất cả tượng trưng cho nhà cái đáng tin tưởng đối với những ai ước muốn thu lợi bằng đặt cược trực tuyến.

FB88 chính là một trong một trong những nhà cái uy tín nhất hiện tại kèm theo các gói khuyến khích hấp dẫn như trả lại cược nhiều ván 100% và tặng 150% nếu tham gia không gian trò chơi may rủi.

5 Tiêu Chí Đánh Giá Nhà Cái Uy Tín

Trò chơi đẳng cấp: Được phát hành bởi các đơn vị phát triển hàng đầu, đảm đương kết quả ngẫu nhiên và không tồn tại sự tác động.

Dịch vụ CSKH: Đoàn chăm sóc người chơi chuyên nghiệp, yểm trợ liên tục bằng nhiều phương tiện.

Trao vượt trội: Mức độ tặng lôi cuốn và dễ dàng thụ hưởng, nhanh chóng rút vốn.

Đảm bảo không rủi ro: Cơ chế bảo vệ tiên tiến, cam kết an toàn chi tiết người sử dụng.

Ngăn ngừa gian lận: Có biện pháp ngăn ngừa gian lận chi tiết, giữ gìn tài sản khách hàng.

Nếu bạn đang có các vài vấn đề liên quan đến hoạt động cá cược, hãy xem xét chương FAQ trên Trang web uy tín hàng đầu với mục đích tìm hiểu nhiều hơn về các nhà cái và ưu đãi mà họ sở hữu.

metDek

Металлообработка в России по низкой цене, детали и чертежи на заказ https://metalloobrabotka96.ru/

gabDek

Изготовление памятников на могилу https://gabbro-d.ru/

Richardven

Я – частный web-мастер по созданию, продвижению, администрированию и дальнейшей раскрутке сайтов. Как частный вебмастер, с 2009 года занимаюсь созданием, продвижением, администрированием, обучением созданию и продвижению сайтов частный маркетолог

AmaliaJW

Натяжные потолки фото

Richardven

Я – частный web-мастер по созданию, продвижению, администрированию и дальнейшей раскрутке сайтов. Как частный вебмастер, с 2009 года занимаюсь созданием, продвижением, администрированием, обучением созданию и продвижению сайтов частное продвижение сайтов seo

Robertven

просушка потолка http://prosushka-pomeshchenij-v-moskve.ru/

KarsonElilup

zofran 8mg tablet

AmaliaNZ

Натяжные потолки

1winJdksj101knich

1win предоставляет игрокам доступ к широкому ассортименту азартных игр и спортивных ставок с бонусами до 500% на первые депозиты.

1winJksj101knich

Официальный сайт 1win предлагает удобный интерфейс, разнообразие игр и высокие коэффициенты для ставок на спорт.

WilliamHem

https://101-diplom.top/

1winJksj100knich

Скачайте приложение 1win и наслаждайтесь всеми функциями платформы, включая ставки, казино и live-игры прямо с мобильного устройства.

1winJdksj100knich

Присоединяйтесь к 1win и получите доступ к уникальным бонусам, кэшбэку до 30% и множеству акций для азартных игроков.

Brucesoori

https://ddos.market

1winJdksj99knich

Воспользуйтесь промокодом при регистрации на 1win и получите 100% бонус на первое пополнение счета.

1WinMes99nuP

Попробуйте удачу в казино 1win с живыми дилерами и множеством азартных игр, доступных круглосуточно.

Brucesoori

https://ddos.rentals

TimothyShent

The following is a list of white defendants executed for killing a black victim. Executions of white defendants for killing black victims are rare execute blacks

1winJdksj98knich

На платформе 1win доступны ставки на более чем 30 видов спорта, включая футбол, баскетбол, теннис и киберспорт.

1WinMes98nuP

Используйте зеркало 1win для безопасного и стабильного доступа к вашему аккаунту, даже если основной сайт недоступен.

TimothyShent

The following is a list of white defendants executed for killing a black victim. Executions of white defendants for killing black victims are rare execute lesbians

Williamhah

карты с пин кодом с деньгами

Невидимый интернет, тайная часть онлайн-пространства, известен с присущими подпольными рынками, куда можно найти объекты и услуги, которые нельзя достать законным способом.

Одним этих продуктов представляют карты с денежными средствами, что выставляются на продажу мошенниками по ценам, существенно дешевле их первоначальной цены.

Для многих потребителей, намеревающихся быстро обогатиться, мысль купить пластиковую карту с остатком на нелегальном рынке может показаться интересной.

Вместе с тем за этими операциями кроются существенные проблемы и нормативные результаты, о которых очень важно быть в курсе.

Каким образом работают предложения по получению банковских карт с денежными средствами?

На теневом рынке можно найти множество предложений о продаже платёжных карт с денежными средствами. Данные карты представляют собой как предоплаченными, так и привязанными с банковскими счетами, и на них, по заявлениям, заранее аккумулированы финансовые средства

Как правило источники заявляют, будто бы платёжная карта имеет определенную количество, которую допустимо использовать для совершения покупок либо получения денег посредством банкоматов.

Цена на такие карты может колебаться в соответствии с в соответствии с декларированного количества денег и с типа пластиковой карты. Например, платёжную карту с остатком $5000 способны предлагать по цене $500, что именно значительно ниже первоначальной стоимости.

Даркнет, скрытая часть глобальной сети, популярен с их противозаконными рынками, в которых предлагаются услуги и услуги, что именно нельзя приобрести открыто.

Одним из подобных товаров являются пластиковые карты с деньгами, что именно выставляются на продажу преступниками по тарифам, существенно меньшие их номинальной стоимости приобретения.

Для ряда потребителей, стремящихся быстро увеличить свои доходы, предложение получить банковскую карту с деньгами на подпольном рынке может казаться заманчивой.

Тем не менее за этими операциями кроются существенные опасности и правовые результаты, касательно которых важно осведомляться.

Каким образом действуют предложения по достанию карт с остатком?

На нелегальном рынке предлагаются множество различных предложений о продаже платёжных карт с остатком. Подобные платёжные карты могут быть как авансовыми, а также привязанными с банковскими счетами, и на них, как декларируется, ранее зачислены денежные средства.

Обычно реализаторы утверждают, что пластиковая карта имеет определенную величину, которую можно расходовать для покупок либо снятия наличности из банкоматов.

Цена на эти карты может колебаться в зависимости от от декларированного количества денег и с разновидности банковской карты. Так, банковскую карту с деньгами $5000 могут предлагать по стоимости $500, что именно заметно меньше номинала.

Предложения по достанию таких карт обычно сопровождаются “”уверениями” от имени реализаторов, которые именно утверждают, якобы пластиковая карта обязательно станет работать, и при этом обещают помощь при возникновении наступления сложностей. Вместе с тем на самом деле такие “”обещания” не очень многое ценность на просторах даркнета, в котором транзакции заключаются анонимно, в связи с чем приобретающий по сути ничем не имеет защиты.

Предложения о покупке подобных платёжных карт типично сопровождаются “”уверениями” от лица реализаторов, что сообщают, будто карта точно окажется функционировать, а также предоставляют помощь в случае возникновения неполадок. Но фактически такие “гарантии” мало что ценность в сфере теневого интернета, в котором сделки заключаются без раскрытия личности, и приобретающий практически никак не имеет защиты.

CarlosNus

Melbet Casino je idealnim mistem pro vsechny milovniky online hazardnich her. Nabizi siroky vyber hernich automatu a slotu, ktere uspokoji jak zacatecniky, tak zkusene hrace. S pestrou nabidkou her a pravidelnymi bonusy je to jedno z nejlepsich kasin na trhu. Uzivatele mohou tezit z vysoke kvality grafiky a plynuleho herniho zazitku, ktery Melbet Casino poskytuje. Pripojte se a objevte nekonecne moznosti, ktere toto kasino nabizi! Zaregistrujte se jeste dnes a vyuzijte uvitaci bonus.

AmaliaCI

Натяжные потолки на кухню

Richardagize

Подпольный интернет, скрытая часть интернета, знаменит своими противозаконными рынками, в которых имеются продукты и сервисы, что не получится приобрести открыто.

Одним этих услуг представляют собой пластиковые карты с балансом, что именно выставляются на продажу нарушителями за стоимость, намного более дешевле их первоначальной стоимости приобретения.

Среди большинства пользователей, желающих быстро стать богатыми, предложение достать карту с деньгами на подпольном рынке может выглядеть заманчивой.

Вместе с тем за этими операциями кроются существенные опасности и правовые итоги, о которых необходимо быть в курсе.

Каким путём работают объявления о продаже по получению пластиковых карт с денежными средствами?

На теневом рынке доступны множество различных объявлений о продаже банковских карт с денежными средствами. Такие пластиковые карты представляют собой в виде предоплаченными, так и ассоциированными с банковскими счетами, и на них, по заявлениям, предварительно аккумулированы деньги.

Типично продавцы утверждают, будто бы платёжная карта включает определенную сумму, которую можно применять в целях совершения покупок а также изъятия наличных с использованием банкоматов.

Цена на подобные пластиковые карты может колебаться исходя из с декларированного остатка а также вида пластиковой карты. Так, платёжную карту с остатком $5000 имеют возможность реализовывать по стоимости $500, что значительно ниже реальной стоимости.

JavierElilup

pioglitazone hcl

BaccaratKdjfn370Hieli

Join a Baccarat site where you can enjoy seamless gameplay with high-quality graphics and realistic sound effects.

BaccaratKdjfn370Hieli

Discover a Baccarat site that offers 24/7 live dealer games, ensuring you never miss a chance to play.

BaccaratKdjfn3769Hieli

Play on a Baccarat site that caters to all levels, from beginners to seasoned professionals.

CarlosNus

Melbet Casino je idealnim mistem pro vsechny milovniky online hazardnich her. Nabizi siroky vyber hernich automatu a slotu, ktere uspokoji jak zacatecniky, tak zkusene hrace. S pestrou nabidkou her a pravidelnymi bonusy je to jedno z nejlepsich kasin na trhu. Uzivatele mohou tezit z vysoke kvality grafiky a plynuleho herniho zazitku, ktery Melbet Casino poskytuje. Pripojte se a objevte nekonecne moznosti, ktere toto kasino nabizi! Zaregistrujte se jeste dnes a vyuzijte uvitaci bonus.

газовые генератор generac

Как не ошибиться при покупке генератора Generac, как выбрать генератора Generac.

Почему стоит выбрать генератор Generac?, анализ генератора Generac.

Как получить бесперебойное электроснабжение с помощью генератора Generac, рекомендации.

Новейшие технологии в генераторах Generac, рассмотрение функционала.

Почему генераторы Generac так популярны?, характеристики.

Как правильно выбрать генератор Generac для своих нужд?, подробный гайд.

Генератор Generac: лучший источник резервного питания, плюсы использования.

Секреты правильного выбора генератора Generac, подробный обзор.

Выбор генератора Generac: на что обратить внимание?, особенности использования.

Как выбрать генератор Generac для вашего дома?, характеристики.

generac генератор купить generac генератор купить .

BaccaratKdjfn369Hieli

Explore a Baccarat site with a user-friendly interface, making it easy to place bets and follow the game.

газовый генератор generac 7189

Как не ошибиться при покупке генератора Generac, как выбрать генератора Generac.

В чем отличие генератора Generac от других моделей?, анализ генератора Generac.

Как получить бесперебойное электроснабжение с помощью генератора Generac, советы по использованию.

Новейшие технологии в генераторах Generac, подробный обзор.

Почему генераторы Generac так популярны?, обзор.

Эффективное решение для энергетической безопасности: генераторы Generac, подробный гайд.

Надежный источник электропитания: генераторы Generac, рассмотрение преимуществ.

Секреты правильного выбора генератора Generac, подробный обзор.

Выбор генератора Generac: на что обратить внимание?, особенности использования.

Как выбрать генератор Generac для вашего дома?, характеристики.

генератора generac https://generac-generatory1.ru/ .

BaccaratKdjfn368Hieli

Choose a Baccarat site with secure payment options and fast withdrawals, so you can focus on the game.

BaccaratKdjfn3768Hieli

Enjoy exclusive bonuses and promotions on a Baccarat site dedicated to rewarding its players.

Patrickhix

купить права категории в

Даркнет, искони превратился узнаваем в виде точка, в пределах которой позволено достать практически любые предметы и опции, не исключая подобные, что располагаются за ограничениями закона.

Одним вариантом аналогичных нелегальных предложений представляет собой возможность приобрести документы категории “В” согласно глобальной классификации — категория “В”).

Значительное число людей, намеревающиеся миновать официальных проверок либо пренебречь предписания, анализируют шанс достать документы типа “В” на даркнете.

При этом такая приобретение связана с многочисленными угрозами а также нормативными итогами, что могут оказаться гораздо сложнее, в отличие от обычная безуспешная приобретение.

AmaliaPK

Натяжные потолки на кухню

MarvinKen

Dưới đây là văn bản với các từ được thay thế bằng các cụm từ đề xuất (các từ đồng nghĩa) được đặt trong dấu ngoặc nhọn :

Hàng đầu 10 Đơn vị tổ chức Đáng tin cậy Bây giờ (08/2024)

Chơi game online đã biến thành một trào lưu rất phổ biến tại nước ta, và việc lựa chọn nhà cái uy tín là chuyện rất cần thiết để đảm đương cảm giác chơi game bảo đảm và công minh. Ở dưới là danh sách Top 10 nhà cái đáng tin cậy được ưa chuộng nhất ngày nay, được phổ biến bởi trang nhận định hàng đầu Top10VN.

ST666 được xem là một trong những nhà cái lớn kết hợp với đáng tin tưởng được ưa chuộng nhất hiện tại. Với chăm sóc khách hàng vượt trội, trợ giúp liên tục kết hợp các dịch vụ khuyến khích đặc sắc tương tự như tặng 110% nếu tạo tài khoản lần đầu tiên, tất cả nhất định là sự chọn lựa hàng đầu dành cho người tham gia.

RGBET nổi bật hơn với gói bảo đảm cược thua thể thao tới 28,888K, kèm theo bồi thường máy đánh bạc 2% mỗi ngày. RGBET là sự lựa chọn vượt trội với những ai yêu thích đánh bạc thể thao và trò chơi đánh bạc.

KUBET có tiếng cùng với cơ chế an ninh vượt trội và server chuyên biệt, yểm trợ bảo vệ tối đa dữ liệu người sử dụng. Nhà cái này cung ứng nhiều ưu đãi khuyến khích lôi cuốn giống như gửi tiền lần hai, khuyến mãi 50%.

BET365 đại diện cho nhà cái chơi game thể thao vượt trội trên khu vực châu Á, nổi bật hơn với các tỷ lệ kèo châu Á, cược tài xỉu và trực tuyến thể thao. Nó chính là sự chọn lựa lý tưởng dành cho những ai mê mẩn đặt cược thể thao.

FUN88 không đơn thuần sở hữu tỷ suất tặng lôi cuốn đồng thời đưa ra đa dạng ưu đãi khuyến khích vượt trội giống như trao 108K Freebet và chứng chỉ cược thể thao SABA lên đến 10,888K.

New88 thu hút người tham gia với các ưu đãi khuyến mãi lôi cuốn như trả lại 2% không hạn chế và tặng phần thưởng mỗi ngày. Tất cả là một trong những nhà cái vừa thu hút nhiều sự quan tâm của người sử dụng cá cược.

AE888 nổi bật hơn kèm theo dịch vụ thưởng 120% lần khởi đầu ký quỹ đá gà

Vâng, tôi sẽ tiếp tục từ đoạn cuối của văn bản:

AE888 nổi bật hơn kèm theo dịch vụ trao 120% lần đầu tiên nạp đấu gà và các chương trình khuyến mãi hấp dẫn khác biệt. Chúng tượng trưng cho nhà cái chuyên biệt cung ứng không gian SV388.

FI88 lôi cuốn người tham gia với mức độ hoàn lại cao kèm theo các dịch vụ ưu đãi gửi tiền lôi cuốn. Đây tượng trưng cho chọn ra tuyệt vời với những người mê mẩn trò chơi bài và slot.

F8BET vượt trội với gói tặng nạp đầu tiên nhận được 8,888,888 VNĐ kèm theo với nhà quản lý phần thưởng 60%. Tất cả tượng trưng cho nhà cái đáng tin với tất cả mong muốn làm giàu dựa trên cá cược qua mạng.

FB88 là một trong những nhà cái đáng tin tưởng số một hiện tại kèm theo các ưu đãi khuyến khích đặc sắc như bồi thường cược xâu 100% và ưu đãi 150% đương góp mặt sảnh chơi jackpot.

5 Tiêu Chí Đánh Giá Nhà Cái Uy Tín

Game tuyệt vời: Được đưa ra cung cấp bởi các nhà cung cấp uy tín nhất, đảm bảo kết cục không lường trước được và không có sự tác động.

Phục vụ chăm sóc người chơi: Đội ngũ hỗ trợ khách hàng chuyên nghiệp, phục vụ 24/7 qua đầy đủ kênh liên lạc.

Thưởng hấp dẫn nhất: Tỷ lệ thưởng hấp dẫn nhất và thuận tiện thực hiện, đơn giản rút ra.

Cam kết đảm bảo: Cơ chế bảo vệ hiện đại, đảm bảo giữ gìn chi tiết người chơi.

Bảo vệ khỏi gian lận: Có cách thức chống gian lận minh bạch, bảo vệ ưu đãi người chơi.

Nếu bạn đang có bất kỳ thắc mắc nào trải nghiệm đánh bạc, hãy xem xét mục FAQ trên Top10VN nhằm mục đích học hỏi chi tiết hơn trong các nhà cái kết hợp với chương trình mà họ cung cấp.

RussellDox

Развитие мессенджеров, таких как Telegram, пользователи теневого интернета нашли новые методы контакта. Телеграм, прославленный своей политикой конфиденциальности и умением построения закрытых чатов, вырос распространенным промежду тех, кто ищет безымянность и безопасность.

На этих каналах можно приобрести рекламу про торговле наркотиков, фальшивых документов, боеприпасов и разнообразных нелегальных артикулов. Отдельные каналы кроме того предоставляют сведения про методах получить доступ к даркнет-сайтам, об эксплуатации безопасного обозревателя либо же как обеспечить инкогнито во онлайн-пространстве.

В большинстве случаев такие группы закрыты, и с целью получения доступа на ним требуется приглашение или соблюдение установленных требований.

В отличие от закрытых онлайн-площадок, каналы теневого интернета на Telegram проще для пользования и не предполагают развертывания дополнительных инструментов. Пользователи имеют возможность проходить к материалам и возможностям напрямую с помощью Телеграм, что превращает указанные каналы более легкодоступными со стороны обширной целевой группы. Однако, аналогично и в случае в теневыми интернет-ресурсами, задействование таких каналов связано с повышенными рисками.

Raymonddew

Anti-Money Laundering Procedures – is a key method deployed by banks and commercial entities to verify that companies do not engaging with separate citizens or organizations involved in illegal activities.

This process involves confirming the identities of buyers by means of various records, such as sanctions records, high-profile individuals (PEP) inventories and further control lists. In the context of the realm of digital currencies, Anti-Money Laundering analysis tools ensure detect and mitigate risks associated with hypothetical illicit money transfers operations.

When performing Anti-Money Laundering analysis, service providers typically consider the specified aspects:

Identity Verification – establishing the credentials of the citizen or company engaged in the operation, to ensure the fact organizations do not included in any oversight lists.

Transaction Models – examining and evaluating operation characteristics for identification of some suspicious activity having can demonstrate illegal financial activities.

Tracing Crypto Assets – applying crypto network analysis means to track the transactions of virtual assets and determine possible contacts to unlawful activities.

AML screening is not a one-time check. It constitutes a continuous procedure aimed at facilitates provide that enterprises uphold compatible with regulations and do not unknowingly participate in criminal activities. Regular Anti-Money Laundering monitoring online activities ensure businesses to update buyer materials and be updated concerning potential transformations in their risk level.

The Functions of Online Anti-Money Laundering Monitoring Systems

AML check online services act as tools which give automated Anti-Money Laundering monitoring systems. Such instruments exceptionally essential for enterprises acting in the decentralized finance context, due to the fact that the likelihood of encountering with illicit funds is higher as a result of the anonymous structure of decentralized money.

RestKGKd19amurn

Откройте для себя ресторан в центре Москвы, где сочетаются изысканная кухня, стильный интерьер и уютная атмосфера. Идеальное место для деловых встреч и романтических ужинов.

RamonFut

https://trespor.com/

HelenOJ

Натяжные потолки в спальню

BaccaratKdjfn367Hieli

Get the most out of your gaming experience on a Baccarat site that offers both traditional and modern variations of the game.

Rodneyror

https://krovinka.com/

BaccaratKdjfn366Hieli

Play on a Baccarat site that prioritizes fair play and transparency, ensuring a trustworthy gaming environment.

SergioElilup

augmentin 750/250mg over the counter

EdwardElilup

navigoi tälle sivustolle

HelenUI

Фото натяжных потоков в спальне

WillieRek

Интернет-аптека работает круглосуточно, поэтому наши клиенты имеют возможность уточнить список имеющихся препаратов с определенным действующим веществом https://alefmex.ru

arenda_zgMt

Лучший выбор для аренды автобуса в Санкт-Петербурге, автобус для экскурсии.

Выгодные предложения на аренду автобуса в Санкт-Петербурге, делайте выбор нашими услугами.

Лучшие автобусы для аренды в СПб, езжайте с комфортом.

Организуйте праздник с нашим автобусом в СПб, с легкостью.

Удобный трансфер в Санкт-Петербурге на автобусе, комфортно и недорого.

Аренда автобуса для корпоративного мероприятия в СПб, профессионально и креативно.

Индивидуальный тур на арендованном автобусе по СПб, познавательно и интересно.

Экскурсионный автобус для школьников в СПб, интересно и разнообразно.

Аренда автобуса для свадьбы в СПб, стильно и празднично.

Как выбрать автобус для аренды в СПб, важные рекомендации от наших экспертов.

Способы сэкономить на аренде автобуса в Санкт-Петербурге, со всеми выгодами.

Что входит в стоимость аренды автобуса в Санкт-Петербурге, подробно изучите перед заказом.

Преимущества аренды автобуса с шофером в Санкт-Петербурге, подробное сравнение.

Стоимость аренды автобуса в СПб – на что обратить внимание, подробное рассмотрение.

Аренда минивэна в СПб для небольших групп, легко и практично.

Аренда транспорта для фестиваля в Санкт-Петербурге, под музыку и веселье.

Вечеринка на автобусе в СПб

аренда микроавтобуса спб https://arenda-avtobusa-v-spb.ru/ .

gabDek

Обслуживание и ремонт ПТО в компании СоюзЭнерго https://remont-pto.ru/

WillieRek

Интернет-аптека работает круглосуточно, поэтому наши клиенты имеют возможность уточнить список имеющихся препаратов с определенным действующим веществом https://almaztravel.ru

arenda_mhOt

Прокат техники для строительства в столице, с гарантией качества.

Выбор экскаватора-погрузчика в Москве, для вашего удобства.

Лучшие компании по аренде спецтехники в столице, находится здесь.

Аренда экскаватора-погрузчика – это просто, под заказ в Москве.

Оптимальные условия аренды спецтехники, заказывайте у нас.

Как выбрать технику для строительства, у нас в сервисе.

Гибкие условия проката техники, заказывайте доступную технику.

Советы по выбору техники для строительства, под заказ у нас.

Выбор оптимального проката техники, в Москве.

Выбор качественного проката, в столице.

Опытные специалисты по технике, в столице.

Основные критерии при выборе техники, в Москве.

Аренда экскаватора-погрузчика в Москве: лучшие предложения, в столице.

Какие условия аренды экскаватора-погрузчика в Москве?, у нас в сервисе.

Современные возможности аренды, в столице.

Быстрая аренда техники по доступной цене, в столице.

Выбор техники для строительных работ, в Москве.

Услуги по аренде техники в столице, в Москве.

аренда трактора с ковшом цена https://arenda-ekskavatora-pogruzchika197.ru/ .

ProjDrsdfglEdica

Simplify your projects and boost productivity with easy-to-use project management software.

arenda_syKl

Оптимальный вариант аренды автобуса в СПб|Аренда автобуса в СПб – залог комфортной поездки|Найдите идеальный автобус для вашей поездки по СПб|Найдите лучшие предложения по аренде автобусов в Санкт-Петербурге|Аренда автобуса для праздника в СПб – идеальное решение|Быстрая и удобная аренда автобуса в СПб|Отправляйтесь в увлекательное путешествие на арендованном автобусе|Идеальное решение для корпоративного транспорта в СПб|Аренда автобуса для свадеб в СПб|Комфортный и безопасный транспорт – наши автобусы в аренде в СПб|Автобусы с кондиционером и Wi-Fi в аренде в СПб|Интересные экскурсии и поездки на арендованном автобусе в СПб|Экономьте на поездках по Санкт-Петербургу с нашими специальными предложениями на аренду автобуса|Индивидуальные маршруты на арендованном автобусе в СПб|Надежная и оперативная поддержка для клиентов аренды автобусов в СПб|Необычайное удовольствие от поездок на арендованных автобусах в СПб|Гибкая система тарифов на аренду автобуса в СПб|Легальная аренда автобусов в СПб|Интересные предложения для аренды автобуса в СПб|Быстрая и удобная аренда автобуса в СПб

аренда автобуса https://arenda-avtobusa-178.ru/ .

BradleyElilup

prestamo 7000 euros

WillieRek

Следует учитывать нормы Жилищного кодекса, которые регламентируют соблюдение порядка и прав соседних жильцов. Для более детального ознакомления с правами жильцов можно ознакомиться с изменениями в законодательный акт, регулирующий жилищные правоотношения, от 20 марта 2024 год https://ariadna-travel.ru

WillieRek

Следует учитывать нормы Жилищного кодекса, которые регламентируют соблюдение порядка и прав соседних жильцов. Для более детального ознакомления с правами жильцов можно ознакомиться с изменениями в законодательный акт, регулирующий жилищные правоотношения, от 20 марта 2024 год https://afrika-afrika.ru

CarlosNus

#file:C:\Users\Администратор\Desktop\xrumer\Texts\texts.txt

CarlosNus

Скидка 20% на все услуги!

Не пропустите! Скидки на наши товары!

Акция! Специальные предложения только сегодня!

CarlosNus

Теперь, когда вы знаете правильный синтаксис, XRumer будет случайным образом выбирать строки из вашего файла для каждого нового сообщения или комментария, что обеспечит разнообразие контента. Если у вас возникнут ещё вопросы или потребуется помощь с дальнейшей настройкой, дайте знать!

CarlosNus

Привет! Мы предлагаем лучший Ваша ссылка тут в городе.

CarlosNus

Tato platforma umoЕѕЕ€uje sГЎzenГ na rЕЇznГ© sportovnГ udГЎlosti. MЕЇЕѕete se tД›ЕЎit na vysokГ© vГЅhry a ЕЎirokou nabГdku her. K dispozici jsou rЕЇznГ© zpЕЇsoby vkladЕЇ a vГЅbД›rЕЇ, kterГ© jsou bezpeДЌnГ© a rychlГ©. Tento web nabГzГ takГ© virtuГЎlnГ sporty a e-sporty. Registrace je jednoduchГЎ a rychlГЎ, takЕѕe mЕЇЕѕete zaДЌГt sГЎzet bД›hem nД›kolika minut. Melbet Casino PortГЎl poskytuje ЕЎtД›drГ© bonusy a promoakce. MЕЇЕѕete sledovat ЕѕivГ© pЕ™enosy a zГЎroveЕ€ sГЎzet na vГЅsledky. ZГЎkaznickГЎ podpora je dostupnГЎ 24/7, aby vГЎm pomohla s jakГЅmikoli problГ©my. Platforma pravidelnД› pЕ™idГЎvГЎ novГ© hry do svГ© nabГdky. Registrace vГЎm otevЕ™e pЕ™Гstup k Е™adД› skvД›lГЅch her a vГЅhod. Tento web nabГzГ pЕ™Гstup k ЕЎirokГ© ЕЎkГЎle sportovnГch udГЎlostГ a kasinovГЅch her. SГЎzenГ v reГЎlnГ©m ДЌase je jednou z hlavnГch vГЅhod tГ©to platformy. Tento online portГЎl nabГzГ hry od pЕ™ednГch svД›tovГЅch poskytovatelЕЇ. MЕЇЕѕete sГЎzet na svГ© oblГbenГ© tГЅmy a sportovce. UЕѕivatelГ© si mohou uЕѕГt rЕЇznГ© kasinovГ© hry s vysokГЅmi vГЅhrami. Na tГ©to strГЎnce najdete skvД›lГ© kurzy pro vЕЎechny hlavnГ sporty. V nabГdce jsou takГ© rЕЇznГ© bonusy pro novГ© i stГЎvajГcГ hrГЎДЌe. Platforma poskytuje ЕѕivГ© pЕ™enosy zГЎpasЕЇ, coЕѕ zvyЕЎuje zГЎЕѕitek ze sГЎzenГ. KaЕѕdГЅ den jsou k dispozici novГ© sГЎzkovГ© pЕ™ГleЕѕitosti. Platforma je dostupnГЎ takГ© v mobilnГ verzi, takЕѕe mЕЇЕѕete sГЎzet odkudkoli.

CarlosNus

Portal poskytuje stedre bonusy a promoakce. Platforma je dostupna take v mobilni verzi, takze muzete sazet odkudkoli. Tento online portal nabizi hry od prednich svetovych poskytovatelu. Uzivatele si mohou uzit ruzne kasinove hry s vysokymi vyhrami. Tento web nabizi pristup k siroke skale sportovnich udalosti a kasinovych her. K dispozici jsou ruzne zpusoby vkladu a vyberu, ktere jsou bezpecne a rychle. Tato platforma umoznuje sazeni na ruzne sportovni udalosti. Zakaznicka podpora je dostupna 24/7, aby vam pomohla s jakymikoli problemy. Tento web nabizi take virtualni sporty a e-sporty. Platforma poskytuje zive prenosy zapasu, coz zvysuje zazitek ze sazeni. Melbet Casino Registrace vam otevre pristup k rade skvelych her a vyhod.

CarlosNus

Portal poskytuje stedre bonusy a promoakce. Melbet Kazdy den jsou k dispozici nove sazkove prilezitosti. Muzete sazet na sve oblibene tymy a sportovce. Muzete sledovat zive prenosy a zaroven sazet na vysledky. Registrace je jednoducha a rychla, takze muzete zacit sazet behem nekolika minut. Zakaznicka podpora je dostupna 24/7, aby vam pomohla s jakymikoli problemy. Registrace vam otevre pristup k rade skvelych her a vyhod. Tento web nabizi pristup k siroke skale sportovnich udalosti a kasinovych her. Platforma pravidelne pridava nove hry do sve nabidky. Tento online portal nabizi hry od prednich svetovych poskytovatelu.

BaccaratKdjfn365Hieli

Enjoy the elegance of Baccarat site that offers both classic and modern game variations.

BaccaratKdjfn3767Hieli

Find the best odds and exciting bonuses on a top-rated Baccarat site.

Glennliz

It would seem that Maltese taxation is quite severe and the corporate income tax rate does not suggest that Malta is a low tax jurisdiction. However, this is not the case. The fact is that non-resident companies in Malta are entitled to a refund of taxes paid, which allows us to talk about the lower level of taxation in Malta compared to most countries in the world.

In order to claim a corporate income tax refund, a foreign company must be registered in Malta as a trading or holding company (deriving its income from trading activities or from participation in other organisations, respectively).

In the tax accounting of a Maltese company, the income earned by it must be recorded in one of four tax accounts: “foreign profits”, “Maltese profits”, “profits from immovable property”, “non-taxable income”. Each type of income is taxed according to its own rules. The final amount of tax is recorded in the fifth account “final tax”.

Example. Consider the two most common cases: a Maltese company derives profits from trading activities abroad and from participation in other companies. In either case, these profits are subject to statutory tax at 35 per cent, but the Maltese shareholders are entitled to claim a refund of the tax taken from the dividends distributed. The refund rules differ for different types of income.

If a Maltese company derives income from trading activities outside Malta (and the term “trading” includes both the direct purchase and sale of goods and the provision of services), its shareholders are entitled, upon receipt of the dividend, to apply for a refund of 6/7th of the tax previously paid in Malta. Therefore, the effective income tax rate will be 5 per cent.

Stephenfig

Regulated United Europe has over 8 years of experience and has over 200 trustworthy partnerships with reliable banks all over Europe. We highly value partnership and long-term business cooperation, and try to expand our partner network every year. We always move forward and are finding new partnership options within the most progressive and safe EMIs and banks in the European region. Our partners have a high level of professionalism and timely fulfil their obligations.

Stephenfig

https://lebedkashop.ru/

ZanderElilup

credito 8000 euros

HelenYK

Натяжные потолки в спальне цена

gabDek

Дверные замки по низким ценам, много акций, доставка по всей России в магазине https://zamok-na-dver.ru/

CarlosNus

Tento web nabizi take virtualni sporty a e-sporty. Tento online portal nabizi hry od prednich svetovych poskytovatelu. Registrace je jednoducha a rychla, takze muzete zacit sazet behem nekolika minut. Registrace vam otevre pristup k rade skvelych her a vyhod. Muzete sazet na sve oblibene tymy a sportovce. Platforma je dostupna take v mobilni verzi, takze muzete sazet odkudkoli. K dispozici jsou ruzne zpusoby vkladu a vyberu, ktere jsou bezpecne a rychle. Platforma pravidelne pridava nove hry do sve nabidky. Tento web nabizi pristup k siroke skale sportovnich udalosti a kasinovych her. Zakaznicka podpora je dostupna 24/7, aby vam pomohla s jakymikoli problemy. Tato platforma umoznuje sazeni na ruzne sportovni udalosti. Portal poskytuje stedre bonusy a promoakce. Uzivatele si mohou uzit ruzne kasinove hry s vysokymi vyhrami. Melbet Muzete se tesit na vysoke vyhry a sirokou nabidku her. Muzete sledovat zive prenosy a zaroven sazet na vysledky.

Lioneltip

https://www.gemius.ru/

Davidbarce

https://abc-context.ru/

BaccaratKdjfn364Hieli

Play with confidence on a Baccarat site known for its secure platform and fair gameplay.

BaccaratKdjfn3766Hieli

Discover a Baccarat site where high rollers and casual players alike feel at home.

peretyazhka-mebeli-minsk ahmn

Преимущества перетяжки мягкой мебели, Как правильно подобрать материал для перетяжки дивана, которые помогут сделать правильный выбор, которые помогут вам сделать стильный выбор, Плюсы и минусы заказа перетяжки у мастера, Как улучшить комфорт мебели при перетяжке, для создания уютного уголка в доме

перетяжка мягкой мебели перетяжка мягкой мебели .

BaccaratKdjfn363Hieli

Join a Baccarat site with a vibrant community of players and regular tournaments.

BaccaratKdjfn3765Hieli

Experience fast and smooth gameplay on a Baccarat site optimized for all devices.

JaceElilup

du kan prГёve her

Robertdaxia

Gambling licence in Ontario Gambling in Ontario is regulated under strict laws and regulations designed to ensure a fair and safe gambling environment for all p

Moreover, the Supreme Court hears and decides on any action plan of the President of the Republic regarding the constitutionality of any law adopted by the House of Representatives. The jury has unlimited jurisdiction to hear and decide any criminal case from the outset. It is almost only in criminal cases where the penalty, imposed by law for the offence in question, exceeds five years’ imprisonment, that a jury is kept under close review.

Requirements for founders

Substance – Foreign banks pay special attention to the real presence of the company. In many cases, Substance is a prerequisite for starting a partnership. But it is not always the business of a legal person that requires an office. For example, the programmer is operating from home and his entire team is also working remotely. In this case, you should explain how business processes.

Conduct of Business (COB) Rulebook

FREQUENTLY ASKED QUESTIONS

Step 2: Selecting the type of licence

A business plan describing the operating model, marketing strategy and financial projections.

Documents confirming the source of income or financial stability (income certificate, tax return).

The framework for regulating cryptocurrency trading in Singapore is the Payment Services Act (PSA), which came into force in 2020. The PSA provides for a comprehensive approach to regulating various types of payment services, including cryptocurrency trading services. The Monetary Authority of Singapore (MAS) is responsible for licensing and supervision under the Act.

SolomonElilup

zofran 4 mg for sale

HelenZH

Натяжные потолки в ванной

BaccaratKdjfn362Hieli

Elevate your gaming experience with live dealer options on this premium Baccarat site.

BaccaratKdjfn361Hieli

Explore a Baccarat site that offers generous welcome bonuses and ongoing promotions for loyal players.

BaccaratKdjfn360Hieli

Play on a Baccarat site that offers real-time action and an immersive casino experience.

BaccaratKdjfn3764Hieli

Choose a Baccarat site with a sleek design and intuitive navigation for an effortless gaming experience.

HenryWat

https://mostbetpk.app/

BaccaratKdjfn359Hieli

Enjoy exclusive access to VIP tables on a Baccarat site tailored for serious players.

Thomasarorb

1вин вход

BetboomDek

Привет, друзья! Сегодня я хочу поделиться с вами информацией о букмекерской конторе Betboom. Я давно увлекаюсь спортивными ставками, и Betboom стала одним из моих любимых мест для азартных развлечений.

Betboom – это современная букмекерская контора, которая предлагает широкий выбор спортивных событий для ставок. Здесь вы найдете лучшие коэффициенты на футбол, хоккей, теннис, баскетбол и многие другие виды спорта. Кроме того, Betboom предлагает возможность делать живые ставки на матчи, следить за результатами в режиме реального времени и увеличивать свои выигрыши.

Официальный сайт Betboom – https://t.me/s/betboom_promokody, где вы можете зарегистрироваться и начать делать ставки уже сегодня. Кроме того, на сайте вы найдете актуальные промокоды и бонусы, которые помогут вам увеличить свои шансы на победу.

Я лично очень доволен сервисом Betboom. Здесь всегда оперативно выплачивают выигрыши, поддержка работает круглосуточно и готова помочь в любой ситуации. Если вы тоже любите ставить на спорт и ищете надежного букмекера, рекомендую обратить внимание на Betboom. Удачи вам и больших выигрышей!

CharlesTus

Мы — команда специалистов, посвятивших себя поиску лучших домов престарелых. Мы ценим заботу, комфорт и безопасность ваших близких. Наши отзывы и опыт говорят сами за себя. Мы поможем вам сделать правильный выбор, чтобы ваши родные чувствовали себя как дома. Давайте работать вместе https://ты-молодец.СЂС„/

Marcella

สวัสดีครับผู้เล่นทุกท่านที่สนใจเกี่ยวกับ

WM Casino! WM Casino เป็น เว็บไซต์คาสิโนที่มี ความน่าเชื่อถือและได้รับความนิยมจากผู้เล่นมากมายทั่วโลก ทาง WM Casino มี เกมคาสิโนหลากหลายประเภท เช่น

เกมบาคาร่า, รูเล็ต, สล็อต และอื่นๆ ที่จะทำให้คุณสนุกไปกับ ประสบการณ์เล่นเกมคาสิโนออนไลน์ ไม่ว่าคุณจะเป็น นักเล่นมือใหม่หรือมือเก๋าก็สามารถเข้าร่วมสนุกได้ที่นี่

อีกทั้งยังมี โปรโมชั่นและสิทธิพิเศษมากมายที่จะทำให้คุณได้รับ ประสบการณ์ที่ดีที่สุดในการเล่น พร้อมกับระบบการเงินที่มี ความปลอดภัยและระบบการเงินที่รวดเร็ว มาร่วมสนุกกับ WM

Casino วันนี้และสนุกไปกับ เกมคาสิโนที่คุณชื่นชอบได้เลยครับ!

Also visit my website … คาสิโนออนไลน์ เล่นง่าย ได้เงินจริง

Danuta

Engaging and illuminating exploration of the topic.

Your critique was complete and well-supported, furnishing subscribers with a comprehensive insight of the fundamental challenges at possession.

I shall be thrilled to collaborate complementary on this matter.

If you permit, I would cordially invite you to connect with

us on the SBOBET community, whereby we will maintain our deliberation in a further

participatory environment.

My web blog online casino player behavior (mcnamarakorsg.jigsy.com)

Donaldmok

построить дом недорого под ключ цены https://spbstroymax.ru/

MichaelWrede

https://stomatologiya-minsk.ru/

AaronCic

изготовление номеров на автомобиль цена https://dublikaty-gosnomer77.ru/

gabDek

Шины оптом по низкой цене в магазине Шина Стандарт в Екатеринбурге https://shina-standart.ru/

KasonElilup

Payday loans in Arizona

Grady

The world of fierce gaming has undergone a remarkable change in recent years, with the rise of

esports as a global rage . Amidst this rapidly transforming landscape,

one name has emerged as a pathfinder – Spade Gaming.

Spade Gaming is a dominance to be reckoned with, a gaming entity that has

carved out a unique proficiency for itself by blending cutting-edge

progress , strategic insight , and a unyielding commitment to superiority .

Established with the goal of reshaping the boundaries of cutthroat gaming, Spade Gaming has quickly become a emblem of

creativity , driving the domain forward with its

visionary approach and steadfast dedication.

At the essence of Spade Gaming’s triumph lies its steadfast determination on

individual development and crew building. The company has cultivated an environment that bolsters and reinforces its competitors , providing

them with the equipment , mentoring , and assistance they need to accomplish new

pinnacles .

But Spade Gaming’s effect extends far outside of the

constraints of the game intrinsically. The entity has also entrenched itself

as a vanguard in the sphere of information creation, utilizing its deep repository

of masterful specialists to manufacture engaging and

spellbinding coverage that resonates among fans

around the earth .

On top of that , Spade Gaming’s allegiance to social duty and community interaction separates

it unprecedented from its rivals . The entity

has maximized its platform to promote vital crusades ,

tapping into its impact and power to cultivate a consequential impact in the domain of esports and

encompassing more .

As the competitive gaming landscape soldiers on to evolve ,

Spade Gaming commands as a shining prototype of what can be realized

when perspective , inventiveness , and a tireless pursuit of perfection fuse

.

In the age to materialize , as the domain of cutthroat gaming presses forward to captivate aficionados and reshape the means we

invest ourselves with entertainment , Spade Gaming will indisputably remain at the forefront

, spearheading the movement and shaping a novel time in the perpetually morphing

landscape of esports.

Also visit my web page; online casino cybersecurity

DerekGak

Лучшие онлайн казино России 2024

Лучшие онлайн казино России

Davidton

Uplifting Vibes Solely: The Best Herb in Tel Aviv

In a era where caliber of living is becoming increasingly vital, countless are pursuing for holistic ways to relax and enhance their health. In the midst of Israel’s Capital, there’s a place that appreciates every minute and delivers only the finest herb products. Salutations to the Coffee Shop, where the slogan “Positive Atmosphere Only” truly materializes.

For what reason Choose Our Store?

We offer a curated assortment of high-grade marijuana items to satisfy all your requirements:

Prescription Herb: For those seeking therapeutic benefits, our medical cannabis variety is excellent, supplying comfort and calm with carefully picked varieties.

Cali Weed: Imported straight from The Golden State, our California Weed provides the finest of the West Coast to TLV, known for its potent impact and high-quality grade.

Israeli Indoor: Locally cultivated and carefully nurtured, our Israeli Indoor weed is great for those who value Israeli quality.

THC Concentrates: Our THC drops are ideal for those who prefer a more discreet and controlled consumption, offering a potent serving in every drop.

Vape Pens THC: For those on the move, our THC vape devices provide ease and power, assuring a smooth and enjoyable session every time.

Space Cake: Pamper yourself to a stellar adventure with our Space Cake, infused with the ideal ratio of Cannabis Extract for a tastily strong experience.

Weed Gummies: Our THC gummies deliver a tasty and effortless way to enjoy herb, excellent for micro-dosing or a pleasant, scrumptious snack.

CBD Offerings: For those looking for the benefits of weed without the high, our variety of CBD offerings delivers tranquil benefits with none psychoactivity.

How to Buy?

Getting is straightforward and hassle-free through our order channel: @WEED2SMOKE. We offer:

5-Star Rating: Our devotion to quality and customer satisfaction is reflected in our five-star feedback.

No-Cost Delivery: Benefit from our selections sent straight to your door at without extra price.

Around-the-Clock Service: We understand that good vibes aren’t bound to a timetable, which is why we’re here around the clock to cater to your needs.

Enjoy the finest that The White City has to supply in cannabis goods. Whether you’re in need of for prescription alleviation, recreational enjoyment, or merely want to de-stress, we’ve got you covered. Order now and bring those uplifting atmosphere to your place!

Mayra

I have meticulously enjoyed the viewpoints

provided in this reflective blog write-up .

The scribe has adeptly expounded several key notions that resonate with me intensely .

As an devoted advocate of trailblazing corporate

initiatives , I would aim to recommend an solicitation to you to explore the unparalleled chances available at Pragmatic Play .

This fluid firm is at the cutting edge of revolutionary

developments , affording a thriving and edifying

setting for persons who demonstrate a enthusiasm for

preeminence and a resolve to transcend the confines of what is

attainable .

I beseech you to consider this entreaty and

examine the wealth of prospects that are available. Kindly be

at liberty to communicate if you have any wonderments or

would like to discuss in more depth .

Kindest salutations ,

my website :: digital casino

Francine

Wow , what an keen post! I really appreciated reading about your stance on this matter .

It’s unquestionably given me a abundance to contemplate

.

I’d long to be privy to more of your thoughts , if you’re amenable to extending the dialogue .

Incidentally , have you heard of MEGA888 ? It’s an magnificent virtual gaming network with heaps of captivating choices .

I’ve been playing there and the endeavor has

turned out to be phenomenal . Assuming that

you’re seeking a novel way to have some amusement and potentially triumph , I’d emphatically recommend

investigating it out . Permit me apprise if you’re interested and I will give more

particulars!

Here is my web blog – online casino player rewards

Samuelcer

Клининг квартиры после животных Москва https://uborka-zapushchennyh-kvartir.ru/

BrianIcero

https://prodvizhenie-podolsk.ru/

EmilianoElilup

LГҐna 9000 kr

Ethan

Compelling and thought-provoking analysis of the subject matter.

Your evaluation was exhaustive and well-supported, furnishing participants with

a thorough knowledge of the essential issues at grasp.

I may be delighted to communicate more on this content.

If you are amenable, I would kindly persuade you to connect with me

on the SBOBET site, in where we would continue our conversation in a further

responsive domain.

my webpage :: online casino bonuses

Printyhu9Mar

Convert BTC to PayPal with ease and enjoy quick access to your funds.

Michal

I unearthed your blog post to be a engaging and shrewd examination of the contemporary state of the domain .

Your examination of the key changes and barriers encountering enterprises in this sphere was particularly forceful .

As an avid devotee of this topic , I would be pleased to

explore this debate more extensively. If you are keen ,

I would warmly encourage you to embark on the

electrifying opportunities provided at WM CASINO. Our framework

delivers a state-of-the-art and guarded landscape for

connecting with aligned people and procuring a multitude of data to

hone your insight of this shifting field . I eagerly await the likelihood of joining

forces with you in the approaching future

Here is my page … casinno online

PachinkoHwx299Baw

Discover the excitement of Pachinko machines, where every spin brings you closer to winning big.

Pachinkoksdjf388Fem

Step into the world of Pachinko, a game that combines skill and luck in a uniquely captivating way.

Nadia

“‘ การ ปรับตัว ของ Evolution Gaming ‘”

การ ดัดแปลง และ ทันสมัย เป็นเรื่องปกติในโลกของ วิทยาศาสตร์ และธุรกิจ ซึ่ง ‘Evolution Gaming’ เป็นหนึ่งในบริษัทที่สะท้อนแนวโน้มนี้อย่างชัดเจน

Evolution Gaming เป็นบริษัทชั้นนำในอุตสาหกรรม

เกมตามโอกาส ออนไลน์

โดย ถือกำเนิดในปี 2006 และมีการ ขยายอิทธิพล

อย่างต่อเนื่อง จนกลายเป็นหนึ่งในผู้นำด้านการให้บริการ เกมโชคลาภ สดแบบออนไลน์ที่ใหญ่ที่สุดในโลก

ความ ความเจริญก้าวหน้า

ของ Evolution Gaming มาจากการ ดัดแปลง และ เจริญก้าวหน้า นวัตกรรมอย่างต่อเนื่อง บริษัทมีการ ดำเนินการใช้ เทคโนโลยีล่าสุดมาใช้ในการ พัฒนา เกมและการ ออกอากาศสด ผ่านแพลตฟอร์มออนไลน์

ทำให้ผู้เล่นสามารถสัมผัส ประสบการณ์

การเดิมพันแบบ ออนไลน์แบบตัวต่อตัว ได้อย่างสมจริง

นอกจากนี้ Evolution Gaming ยังมีการ

เสริมสร้าง บุคลากรภายในองค์กรอย่างต่อเนื่อง

โดยการ ปรับปรุง ทักษะของ บุคลิกภาพ เพื่อให้สามารถ รับมือ ความต้องการของ ผู้ใช้บริการ ได้อย่างมี

ความครบถ้วน ซึ่งเป็นปัจจัยสำคัญที่ทำให้

Evolution Gaming สามารถ ดำเนินการต่อสู้ และ ก้าวไกล อย่างต่อเนื่องในตลาดที่มีการแข่งขันสูง

การ ปรวนแปร ของ Evolution Gaming ไม่เพียงแต่สะท้อนถึงความ ความเจริญก้าวหน้า ขององค์กรเท่านั้น

แต่ยังเป็นตัวอย่างที่ดีของการ ปรวนแปร และพัฒนา นวัตกรรมในโลกธุรกิจ ซึ่งเป็นปัจจัยสำคัญที่จะนำไปสู่

ความพัฒนา และ ความมั่นคง ในอนาคต

Here is my page: ไซต์คาสิโนออนไลน์;

blogfreely.net,

Karolin

Friendly greetings, comrade subscriber. I encountered your deep feedback on the

blog submission particularly perceptive .

Your position on the subject matter is somewhat admirable .

As you seem to possess a ardent curiosity in the matter

, I desire to deliver an call for you to dive into

the world of ‘918KISS’.

This very hub delivers a extensive assortment of

engaging material that in turn accommodate participants with wide-ranging

passions .

I gather you possibly locate the fellowship at ‘918KISS’ as both valuable

and intellectually stimulating .

I exhort you to mull over joining us and offering

your unparalleled observations to the ongoing dialogues .

Excited for potentially integrating you on board .

Also visit my web page; online casino; barbourmonagh.jigsy.com,

LentaDek

Когда я ищу актуальные промокоды и скидки для покупок в интернет-магазинах, я всегда обращаюсь к Ленте Онлайн. Этот ресурс стал для меня настоящим спасением, ведь здесь собрана самая свежая информация о выгодных предложениях и акциях.

На официальном сайте Ленты Онлайн https://t.me/s/promokodi_lenta я всегда могу найти актуальные промокоды и купоны на различные товары и услуги. Благодаря этому ресурсу я могу сэкономить значительные суммы при покупках онлайн.

Кроме того, на сайте Ленты Онлайн я всегда могу найти информацию о текущих акциях и распродажах в популярных интернет-магазинах. Это помогает мне быть в курсе всех выгодных предложений и не упустить возможность сэкономить на покупках.

Я очень благодарен Ленте Онлайн за то, что они предоставляют такую ценную информацию и помогают мне экономить деньги. Благодаря этому ресурсу я могу делать покупки более осознанно и выгодно. Я всегда рекомендую Ленту Онлайн всем своим друзьям и знакомым, ведь это действительно незаменимый помощник для тех, кто ценит свои деньги.

JohnnycrynC

solara executor

Randalljew

https://prodvizhenie-chelyabinsk.ru/

JamelPak

https://prodvizhenie-mitishi.ru/

PachinkoHwx298Baw

Enjoy the bright lights and fast-paced action of Pachinko, a game that has captivated players for decades.

JustinElilup

basics

Pachinkoksdjf386Fem

Try your hand at Pachinko and see why this popular game has become a cultural icon in Japan.

PachinkoHwx297Baw

Pachinko is more than just a game, it’s an experience that combines excitement, strategy, and fun.

Charis

Remarkable Entry Thoughts

Remarkable , what a profound blog ! I sincerely savored

reading your analysis on this topic .

As an individual who has been following your digital

platform for a stretch, I must convey that this is among your finest expertly

written and enthralling content yet .

The style you integrated various perspectives and

scholarly results was sincerely phenomenal.

I found myself as I read since your points merely

seemed to unfold remarkably seamlessly .

Review my web-site … asia gaming slots

Laurene

Wrapped up Reading a Blog Post: A Formal Input to the Comment Section and an Invitation to Join “KING855”

‘After meticulously reading the blog post, I would like to

furnish the following input to the comment .

Your reflections concerning the subject matter were quite intriguing

. I was in alignment with many of the arguments you mentioned

.

It is heartening to see such an engaging dialogue unfolding.

If you are keen in deeper examining this theme, I would sincerely urge you to become a member of the “KING855” group .

There , you will have the opportunity to engage

with like-minded members and explore further into

these captivating topics .

I am confident your involvement would be

a significant addition to the discussion .

Appreciate your remarks, and I anticipate the possibility of extending this enriching dialogue .

my homepage: online casino deposit bonuses

BillySef

раскрутка сайта

Mitzi

Remarkable , what an keen post! I really enjoyed

reading about your take on this topic . It’s unquestionably given me a

copious amount to consider.

I’d long to listen to more of your reflections , if you’re inclined to

extending the discussion .

By the way , have you learned of MEGA888? It’s an fantastic internet

gaming ecosystem with piles of invigorating selections .

I’ve engaged in there and the endeavor has proved

to be exceptional. Provided that you’re on the hunt for a novel way to enjoy some recreation and feasibly come out on top , I’d emphatically recommend

exploring it further. Permit me know whether you’re eager and

I will offer more particulars!

Look into my site; online casino influencer marketing

Andrewlow

באשקלון הן המקום שאתה רוצה להיות. אתה יודע על מה אנחנו מדברים, בדיוק כפי שאנו יודעים שזה מה שאתה צריך. ואין מה להתבייש או רוצות שהיה לך טוב ונעים. והן גם יודעות איך לעשות זאת בצורה הטובה ביותר. אין סיבה להרגיש לבד כאשר אתה יכול להזמין כבר עכשיו click

Richardupdaw

של תל אביב לפעמים גברים צריכים חוויות קצת יותר פרועות ופחות שגרתיות. גברים כמוך צריכים לשבור את השגרה, ולקבל פינוק חם ולוהט במערכת היחסים הזוגית יותר מכל דבר אחר. כאשר הגבר מגשים את הצרכים המיניים שלו, בין אם זו התנסות עם קוקסינלית או משהו אחר, homepage

Andrewlow

אירוטית דירות דיסקרטיות הן המקום בו כל גבר שואף לבקר בו כאשר הוא רוצה לחוות ולממש את הצרכים הגבריים ולהרגיש את תענוגות הקריות עושים – להזמין נערות ליווי בקריות לבילוי שהוא ליגה אחרת. גברים רבים, צעירים ומבוגרים, מבלים עם נערות הליווי ונהנים great article

PachinkoHwx296Baw

Get hooked on the fast-paced excitement of Pachinko, where every ball can lead to a big win.

Richardupdaw

בין בני זוג. ולא רק בין בני זוג, לעתים נשים וגברים, גברים וגברים או נשים ונשים, מקיימים מפגשים רק למטרת קיום יחסי מין מהם שני זוגו, וזהו חלק מעירור התשוקה המחודשת. כפי שהבנתם ישנן שלוש סיבות טובות מדוע לבקר דירות דיסקרטיות. אבל גם גברים שאין להם מערכת נערת ליווי בתל אביב

Angelo

What an insightful and meditative write-up!

I have to proclaim, your analysis of this crucial

subject was genuinely exceptional .

The extent and subtlety you infused to the discourse

was extraordinary , casting new light on the nuances at hand .

I found myself agreeing as I read through your skillfully crafted points .

The manner you were empowered to extract the core themes excepting streamlining was particularly exceptional.

It’s clear you’ve devoted a great deal of energy

into examining this topic .

This article has presented me a significant amount to

mull over and has challenged me to reassess specific aspects of my personal outlook .

I value you investing the effort to convey your mastery – articles like this are immensely priceless

in progressing the wider dialogue .

I look forward to skimming more of your material in the future to follow.

Please continue the outstanding endeavors !

My site microgaming software systems limited (Eula)

WilderElilup

click for info

PachinkoHwx295Baw

Step into the world of Pachinko, a game that combines skill and luck in a uniquely captivating way.

Pachinkoksdjf383Fem

Find out why Pachinko is one of Japan’s most popular games, offering endless excitement and rewards.

Kali

Astounding , what an discerning post! I really relished reading about your outlook on this topic .

It’s unquestionably given me a copious amount to think about .

I’d yearn to listen to more of your viewpoints, if you’re willing to prolonging the discussion .

Coincidentally , have you heard of MEGA888 ? It’s an magnificent

internet gaming ecosystem with piles of captivating options

. I’ve been playing there and the journey has proved to be

phenomenal . On the condition that you’re seeking a innovative way to

partake in some amusement and conceivably emerge victorious ,

I’d ardently endorse investigating it further. Let me apprise

if you’re eager and I can provide more details !

Take a look at my website :: casino bonuses (Angelina)

orgoDek

Оргстекло по низким ценам в Екатеринбурге https://www.orgsteklo-k66.ru/

Cassie

Remarkable Blog Entry

Gosh , what an thought-provoking and contemplative content!

I found myself nodding along as I read through your examination of this vital topic .

Your assertions were meticulously studied and conveyed in a

concise , convincing manner. I specifically treasured

how you were equipped to refine the core complexities

and complexities at operation , minus oversimplifying or overlooking the obstacles .

This article has provided me a lot to ponder

. You’ve undisputedly widened my understanding

and shifted my perspective in certain significant ways .

Thankfulness for devoting the resources to

disseminate your expertise on this subject .

Posts like this are such a priceless addition to the dialogue .

I anticipate witnessing what other thought-provoking

information you have in supply.

Here is my blog – ebet com register login

PachinkoHwx294Baw

From casual play to competitive strategy, Pachinko provides a gaming experience like no other.

Bradleyunesk

כמו כוכב קולנוע. אם תמיד חלמת להיות הגבר שהבחורות מחכות לו ורוצות לתת לו את כל מה שהן יודעות, אתה יכול להגשים זאת עוד היום. צועד אל עבר עולם של הגשמת פנטזיות ורגעים נעימים במיוחד. כאשר אתה סוגר את הדלת מאחוריך, אתה משאיר את כל הדאגות בחוץ. זוהי סקס דירה

Pachinkoksdjf382Fem

Take a spin on a Pachinko machine and immerse yourself in a game that’s as much about skill as it is about luck.

RonaldCoxia

ליווי בחיפה 24 שעות ביממה, והן מייד יעשו את העבודה. מייד הן יחפשו כיצד לענג ולפנק אותך, ופשוט לגרום לך להרגיש טוב עם עצמך. גוף או כל העדפה שיש לך. תוך זמן קצר הנערה תגיע אלייך, ותעניק לך בילוי חם ולוהט. אתה כבר מתחיל לדמיין את הדברים הלוהטים שתעשו, דירות דיסקרטיות בצפון

AdrianTiemy

ומשחררות. זה כל כך פשוט לחולל שינוי בחייך. שיחת טלפון אחת ומייד תגיע נערה שתיתן מענה לכל החשקים והצרכים גבריים שלך. אתה תרגיש נראה כי אתה חייב לעצמך בילוי שכזה. אם תבקר הערב דירות דיסקרטיות בחולון, אתה תיכנס אל עולם התענוגות שאתה מחפש. זה יעשה לך טוב נערות ליווי בחולון

Lucia

The given subject matter of this blog post is really

intriguing . I delighted in the way you investigated the

different issues so exhaustively and clearly .

You enabled me acquire fresh outlooks that

I had not considered before. I’m grateful for imparting your expertise

and expertise – it has equipped me to gain understanding

additionally .

I particularly relished the ground-breaking outlooks you

revealed, which broadened my awareness and reasoning in significant

directions . This blog is systematic and compelling

, which is paramount for subject matter of this caliber .

I wish to review more of your creations in the times ahead , as I’m assured it

shall continue to be enlightening and facilitate me persist in developing .

I express my gratitude !

Have a look at my site :: video poker; https://hub.docker.com/,

Augustus

Greetings , fellow reader . I discovered your contemplative observations

on the blog write-up remarkably keen .

Your outlook on the matter is quite impressive .

As you sound to bear a ardent investment in the matter , I would extend an invitation for you to explore the domain of ‘918KISS’.

This website offers a comprehensive variety of riveting

offerings that accordingly suit users

possessing multifaceted passions .

I believe you would come across the society at ‘918KISS’ as being equally

beneficial and academically stimulating .

I urge you to contemplate linking up with us and supplying your priceless judgments to the ceaseless debates .

Anticipating potentially embracing you into our

group .

my blog post; online casino minimum deposits, https://peatix.com,

Antoniodrady

באמצעות בילוי עם נערות ליווי ברמת גן. הבחורות היפיפיות יודעות תמיד להרים את מצב הרוח ולגרום לגבר להרגיש טוב. והן יודעות להסיר הדיסקרטיות היא חוויה משחררת המותאמת בדיוק לצרכים של כל גבר. ובימים שכאלו, שבהם כולנו סובלים ממתחים ומלחצים, זהו בדיוק מה helpful resources

nine casino

Se stai cercando un’esperienza di gioco emozionante e sicura, ninecasino e la scelta giusta per te. Con un’interfaccia user-friendly e un login semplice, Nine Casino offre un’ampia gamma di giochi che soddisferanno tutti i gusti. Le nine casino recensioni sono estremamente positive, evidenziando la sua affidabilita e sicurezza. Molti giocatori apprezzano le opzioni di prelievo di Nine Casino, che sono rapide e sicure.

Uno dei punti di forza di Nine Casino e il suo generoso nine casino bonus benvenuto, che permette ai nuovi giocatori di iniziare con un vantaggio. Inoltre, puoi ottenere giri gratuiti e altri premi grazie ai nine casino bonus senza deposito. E anche disponibile un nine casino no deposit bonus per coloro che desiderano provare senza rischiare i propri soldi.

Scarica l’nine casino app oggi stesso e scopri l’emozione del gioco online direttamente dal tuo dispositivo mobile. Il nine casino app download e semplice e veloce, permettendoti di giocare ovunque ti trovi. Molti si chiedono, “nine casino e sicuro?” La risposta e si: Nine Casino e completamente legale in Italia e garantisce un ambiente di gioco sicuro e regolamentato. Se vuoi saperne di piu, leggi la nostra recensione di Nine Casino per scoprire tutti i vantaggi di giocare su questa piattaforma incredibile.

nine casino e legale in italia https://casinonine-it.com/ .

AdrianTiemy

עם נערות המארחות בדירתן. לא לכל גבר יש את האפשרות להזמין את הנערות לביתו, ולכן דירות דיסקרטיות בקריות יכולות להיות הפתרון. בהן פעולה מלא במהלך הגשמת הצרכים המיניים שלהם. ואלו הם דברים שהאישה הממוצעת מתקשה לספק לגבר. לא כל אישה מציגה גוף מושלם. ולא כל read contentsays:

Pachinkoksdjf381Fem

Pachinko offers an addictive mix of luck and strategy, making it a must-try for any gaming enthusiast.

PachinkoHwx293Baw

Enjoy the rush of Pachinko and see if you can hit the jackpot in this electrifying arcade game.

Nannie

Thank Your Thoughts!

I’m Pleased you Encountered the Commentary Informative.

If you’re Enthusiastic about Discovering more Prospects in the online Gambling Sphere, I’d Advise Experiencing CMD368.

They Provide a Myriad of Enthralling Gaming Choices,

Broadcasted events, and a Accessible Interface.

What I Genuinely Admire about CMD368 is their Focus to Ethical Sports.

They have Reliable Security and Tools to Facilitate Participants Manage their actions.

Regardless of whether you’re a Skilled Enthusiast or New to the Betting, I Reckon you’d Sincerely Love the Experience.

Feel free to Become a member Via the Connection and Let me know if you have Further Concerns.

nine casino prelievo

Se stai cercando un’esperienza di gioco emozionante e sicura, ninecasino e la scelta giusta per te. Con un’interfaccia user-friendly e un accesso facile, Nine Casino offre un’ampia gamma di giochi che soddisferanno tutti i gusti. Le recensioni di Nine Casino sono estremamente positive, evidenziando la sua affidabilita e sicurezza. Molti giocatori apprezzano le opzioni di prelievo di Nine Casino, che sono rapide e sicure.

Uno dei punti di forza di ninecasino e il suo generoso nine casino bonus benvenuto, che permette ai nuovi giocatori di iniziare con un vantaggio. Inoltre, puoi ottenere free spins e altri premi grazie ai nine casino bonus senza deposito. E anche disponibile un no deposit bonus per coloro che desiderano provare senza rischiare i propri soldi.

Scarica l’nine casino app oggi stesso e scopri l’emozione del gioco online direttamente dal tuo dispositivo mobile. Il nine casino app download e semplice e veloce, permettendoti di giocare ovunque ti trovi. Molti si chiedono, “nine casino e sicuro?” La risposta e si: Nine Casino e completamente legale in Italia e garantisce un ambiente di gioco sicuro e regolamentato. Se vuoi saperne di piu, leggi la nostra nine casino recensione per scoprire tutti i vantaggi di giocare su questa piattaforma incredibile.

nine casino app download https://nine-casino-italia.com/ .

Franklin

Astounding Blog Thoughts

Impressive , what a compelling entry! I truly enjoyed perusing your insights

on this matter .

As someone who has been tracking your online presence

for a duration , I need to convey that this is alongside your greatest

expertly written and engaging pieces thus far .

The style you intertwined together viewpoints and research

data was really remarkable . I came across myself nodding as I

read because your assertions simply came across to progress remarkably fluidly.

My web page bk8 thai

CadeElilup

zofran 8mg otc

EfrainFrulk

주식

Cathleen

The world of rigorous gaming has undergone a remarkable

evolution in recent years, with the rise of esports as a global phenomenon .

Amidst this rapidly progressing landscape, one name has emerged as a visionary – Spade Gaming.

Spade Gaming is a might to be reckoned with, a gaming company that has carved out a unique

forte for itself by blending cutting-edge invention , strategic foresight ,

and a relentless commitment to prowess.